Decoding Amazon’s P/E, PEG & Profit

If you’ve ever pulled up Amazon’s stock (AMZN) and thought, “Why is this thing always so expensive?”, you’re not alone.

P/E, PEG, revenue, profit margin — it can feel like alphabet soup with a side of anxiety. Let’s break Amazon down like you would a credit card statement after the holidays: line by line, in plain English.

Quick refresher: what are P/E, PEG, revenue, and profit margin?

Before we zoom in on Amazon specifically, let’s make sure the terms are clear.

Price-to-Earnings ratio (P/E)

- P/E = Share price ÷ Earnings per share (EPS)

- Rough idea: how many dollars investors are willing to pay for $1 of current earnings.

- High P/E usually means investors expect strong growth (or the stock is overhyped… or both).

PEG ratio (Price/Earnings to Growth)

- PEG = P/E ÷ expected earnings growth rate.

- A PEG around 1 is often seen as “fairly valued” relative to growth.

- PEG ≫ 1 can mean the stock is expensive for its growth rate.

Revenue

- The total money Amazon brings in from sales (online store, AWS, ads, subscriptions, etc.).

- Think: top line.

Profit margin

- Profit margin = Profit ÷ Revenue.

- Shows how much actual profit Amazon keeps from each dollar of sales.

- Low margin: lots of volume but not much leftover.

- High margin: each sale is very profitable.

P/E and PEG tell you how the market is pricing Amazon’s earnings and growth. Revenue and profit margin tell you how Amazon actually makes and keeps money.

Why Amazon’s P/E ratio is usually high (and why that’s not random)

If you look up AMZN’s P/E on any finance site, you’ll often see a number that looks way higher than old-school value stocks (think banks or consumer staples).

Why?

1. Reinvestment culture

For years, Amazon deliberately ran with thin or near-zero profits in its retail business, constantly plowing money back into logistics, data centers, content, and devices. That made reported earnings low, which pushed the P/E ratio higher.

2. Multiple businesses inside one ticker

Amazon isn’t just an online store:

- E-commerce (low-margin, huge revenue)

- AWS (Amazon Web Services) – high-margin cloud computing

- Advertising – very high-margin, growing fast

- Subscriptions (Prime, etc.)

Markets tend to value these higher-margin, high-growth segments richly, which also supports a higher P/E.

3. Growth premium

Historically, Amazon’s revenue and cash flow growth have been strong, especially in AWS and ads. High growth + strong market position = investors willing to pay up.

So a high P/E for AMZN is less about “Wall Street lost its mind” and more about “Wall Street is paying for the future earnings stream, not just the present.”

A high P/E for Amazon is normal for a mature-but-still-growing tech platform with powerful high-margin segments.

How PEG ratio helps you sanity-check Amazon’s valuation

P/E alone can mislead you.

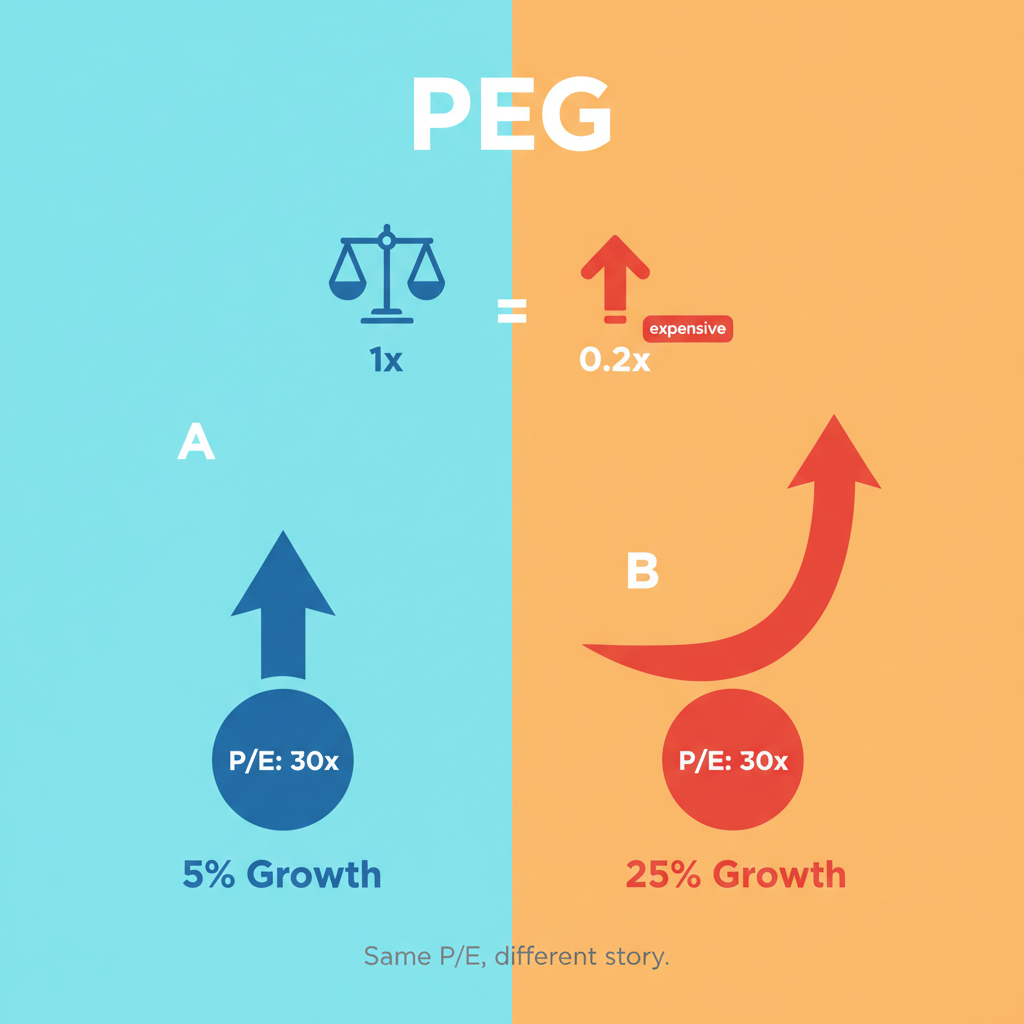

Imagine two stocks:

- Stock A: P/E of 30, growing earnings 5% a year.

- Stock B: P/E of 30, growing earnings 25% a year.

Same P/E, totally different story.

That’s why investors look at PEG:

- PEG ≈ 1: Price roughly in line with expected earnings growth.

- PEG < 1: Potentially undervalued (or growth is overestimated).

- PEG > 1: Potentially overvalued relative to its growth.

For Amazon, PEG tries to answer:

“Given Amazon’s growth prospects (AWS, advertising, AI, logistics, etc.), does the current P/E make sense, or are we overpaying?”

Where PEG becomes tricky

- Growth estimates are just that — estimates.

- Analysts can be too optimistic or too pessimistic.

- Big macro changes (consumer demand, interest rates, regulation) can flip growth expectations.

How to use PEG for AMZN practically

- Look up Amazon’s forward P/E and consensus earnings growth rate.

- Calculate or check its PEG.

- Compare AMZN’s PEG to:

- The broader market (e.g., S&P 500 average PEG)

- Other mega-cap tech names

- Decide: “Am I okay paying this multiple for this level of growth?”

PEG is your “is this growth worth the price?” checkpoint for Amazon.

Amazon’s revenue: massive, but that’s only half the story

Amazon’s revenue is famously huge. But huge revenue does not automatically mean huge profit.

Amazon has multiple revenue streams with very different economics:

1. Online stores (first-party retail)

- Low-margin, price-competitive business.

- Big chunk of revenue, relatively small slice of profit.

2. Third-party seller services

- Fees from independent sellers using Amazon’s marketplace.

- Higher margin than first-party retail, plus recurring.

3. AWS (cloud computing)

- Lower share of revenue compared to retail, but outsized share of operating income.

- Cloud services carry structurally higher margins thanks to software and infrastructure leverage.

4. Advertising

- Sponsored listings and display ads on Amazon’s properties.

- Very high-margin: once the platform exists, extra ad dollars mostly drop to the bottom line.

5. Subscriptions (Prime, etc.)

- Recurring revenue.

- Strengthens customer loyalty and boosts spending in other segments.

If you only look at total revenue, you might miss that much of Amazon’s profit engine lives in AWS and advertising, not the core retail store.

Amazon’s revenue headline is impressive, but the real magic is the mix — where each dollar of revenue comes from.

Profit margin: why Amazon can look “weak” and still be powerful

Historically, Amazon has had thin net profit margins, especially compared with high-margin software giants.

That’s not because Amazon doesn’t know how to earn money — it’s because of strategy.

1. Low-margin retail by design

E-commerce is extremely competitive. Amazon used:

- low prices,

- fast shipping,

- and constant reinvestment

to gain and hold massive market share. This naturally kept margins tight.

2. High-margin segments offset the thin parts

AWS and advertising have much fatter margins, which:

- Lift overall operating margin over time.

- Give Amazon the cash flow to continue investing.

As those higher-margin segments grow faster than core retail, Amazon’s blended margin can improve even if retail stays thin.

3. Margins can expand with scale and discipline

When Amazon tightens costs (logistics, headcount, data center efficiencies) while high-margin areas keep growing, both operating margin and net margin can trend higher.

Amazon’s low overall margin doesn’t mean it’s a bad business — it means you must look under the hood to see which parts create the profit.

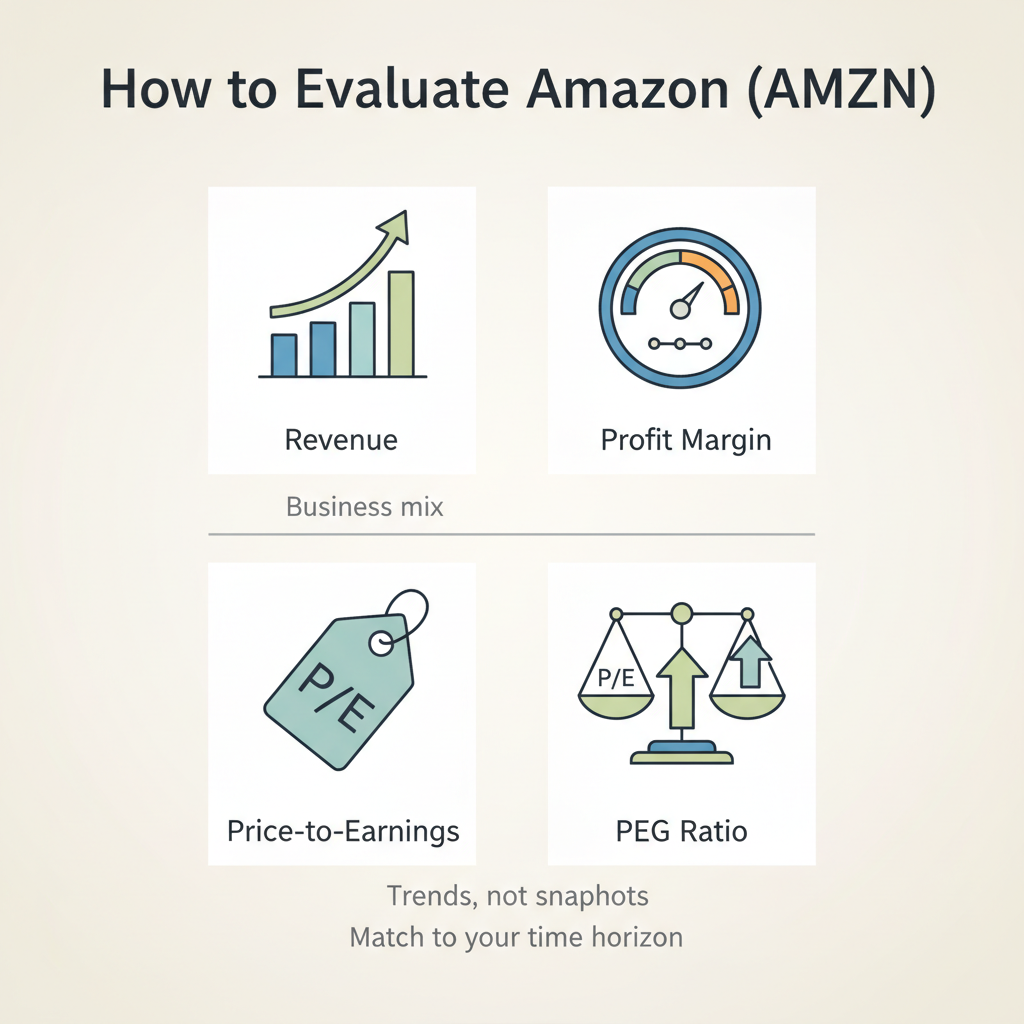

How to look at AMZN without getting overwhelmed

Here’s a simple framework to evaluate Amazon using P/E, PEG, revenue, and profit margin together.

Step 1: Check the business mix

Ask:

- How much of the story is low-margin retail vs high-margin AWS and ads?

- Are AWS and advertising growing faster than the rest of the company?

If high-margin segments keep taking share, that supports margin expansion and may justify a higher P/E.

Step 2: Look at profitability trends, not just one year

Instead of fixating on a single margin number:

- Is operating margin trending up or down over the last few years?

- Is Amazon turning more revenue into operating income and free cash flow?

An improving margin trend plus strong top-line growth is a powerful combo.

Step 3: Use P/E and PEG as context, not gospel

- Compare Amazon’s P/E to its own history and to large tech peers.

- Look at AMZN’s PEG vs:

- S&P 500 average PEG

- Other mega-cap tech names

High P/E + high PEG? You’re paying a premium; you need to really believe in long-term growth.

Moderate P/E + reasonable PEG? Could be a more balanced risk/reward.

Step 4: Match the stock to your timeline

Amazon is a classic long-term compounding story:

- Short term: margins can be noisy due to investment cycles, capex, and macro conditions.

- Long term: the thesis hinges on AWS, advertising, logistics efficiency, and new growth areas (like AI and new services) driving earnings power higher.

If you’re looking at a 6-month window, Amazon’s P/E might just annoy you. If you’re thinking in 5–10 years, the interplay between revenue growth, margin expansion, and valuation becomes more meaningful.

Don’t treat any single metric as a “buy/sell” button. Use them together, in context, and with your own time horizon in mind.

Common mistakes people make with AMZN’s valuation

Mistake 1: Treating Amazon like a pure retailer

Amazon is not just an online store.

If you value AMZN like a grocery chain or a no-growth retailer, you’ll likely misunderstand its earnings potential from:

- AWS,

- advertising,

- and subscription ecosystems.

Mistake 2: Ignoring cash flow

Earnings can be distorted by accounting, stock-based compensation, and heavy investment cycles.

Serious investors often also look at:

- Operating cash flow

- Free cash flow

These can give a clearer picture of what Amazon can actually reinvest, use to reduce debt, or return to shareholders over time.

Mistake 3: Obsessing over a single year’s margin

Amazon’s strategy sometimes means:

- Investing heavily (which compresses margins for a time), then

- Harvesting the benefits later via higher efficiency and revenue.

Seeing margins dip during an investment phase and shouting “broken business!” is usually premature.

A nuanced view of Amazon requires looking at segments, cash flows, and multi-year trends — not just one quarter and a P/E snapshot.

So… is Amazon overvalued or not?

Here’s the most honest answer: it depends on what you believe about its future growth and margins.

To form your own view, ask yourself:

- Do I believe AWS and advertising can keep growing at attractive rates?

If yes, you might be more comfortable with a higher P/E. - Do I think Amazon’s logistics and scale can keep improving margins in retail and services?

If you see operating margin expanding over time, current valuation may feel more reasonable. - What am I assuming about regulation, competition, and cloud pricing?

- Competition from other cloud providers and retailers

- Potential antitrust or regulatory pressures

- What’s my time horizon?

If you need quick returns, a high-valuation, long-duration story like AMZN might not match your goals.

There’s no one-size-fits-all verdict. The real question is whether Amazon’s long-term earnings trajectory justifies the price to you.

Final thoughts: how to keep this simple

When you feel lost in metrics, come back to four core questions:

- Revenue: Is Amazon still growing its top line at a healthy, sustainable clip?

- Profit margin: Are margins stable, rising, or shrinking over several years?

- P/E: Am I comfortable paying this many dollars for each dollar of earnings today?

- PEG: Does the expected growth rate make that P/E feel justified?

If those four answers line up with your risk tolerance and time horizon, then you don’t need to overcomplicate it.

Always remember: P/E, PEG, revenue, and profit margins aren’t there to impress anyone — they’re just tools to help you decide whether AMZN’s story is one you genuinely want to own for the long run.

Leave a Reply